The first thing lenders consider when you apply for a mortgage is your credit score. A lender could immediately decline your application if your score is not high enough. However, even if it is high enough to qualify, it could affect your mortgage in other ways.

Here’s everything you must know about how does credit score affect mortgage rate?

What is a Credit Score?

Your credit score is a number derived from your credit history. The better your credit history, the higher your credit score, and vice versa.

The credit bureaus have an algorithm they use to calculate your credit score based on these factors:

Payment history

Credit utilization

Length of credit history

Credit mix

New credit

Credit scores range from 300 – 850, with 850 being the highest score a person can get. The algorithm depends on the credit model a lender chooses, but they are all similar, giving various weights to the above factors.

Why Do Lenders Care about your Credit Score?

Lenders care about your credit score because it tells them if you pay your bills on time and handle your finances properly. If you have a low credit score, you’re at a higher risk of default, and if you have a higher credit score, you’re at a lower risk of default.

Lenders use your credit score as a first level of determining if you qualify for a mortgage. If your credit score doesn’t meet the loan guidelines, they won’t move forward with your loan.

What ways does credit score affect mortgage rate?

So how does your credit score affect your mortgage? Here’s how.

Mortgage Rates

The largest factor affected by your credit score is the mortgage rates lenders will charge. Your interest rate is based on your risk level. Therefore, the riskier you are, the higher the interest rate a lender will charge.

Loan Requirements

If you have a higher credit score, you may get more lenient mortgage guidelines, such as your down payment. Conversely, if you have a high credit score, you may get approved with a lower down payment than you would if you had a lower credit score.

Your credit score can also serve as a compensating factor for other loan requirements. For example, if you have a higher than normal debt-to-income ratio but a great credit score, a lender may overlook the higher DTI and approve the loan.

Mortgage Insurance

If you put down less than 20% on your home, you’ll pay mortgage insurance on a conventional loan, and your credit score determines how much you pay. But, like interest rates, lenders base your PMI on your riskiness. So if you have a lower credit score, you’re a riskier borrower and must pay more PMI to compensate for the risk.

Loan Fees

Lenders charge loan fees on all loans, but the higher your risk of default is, the more loan fees you’ll pay. So, for example, a borrower with great credit likely won’t pay mortgage points, but a borrower with fair credit will.

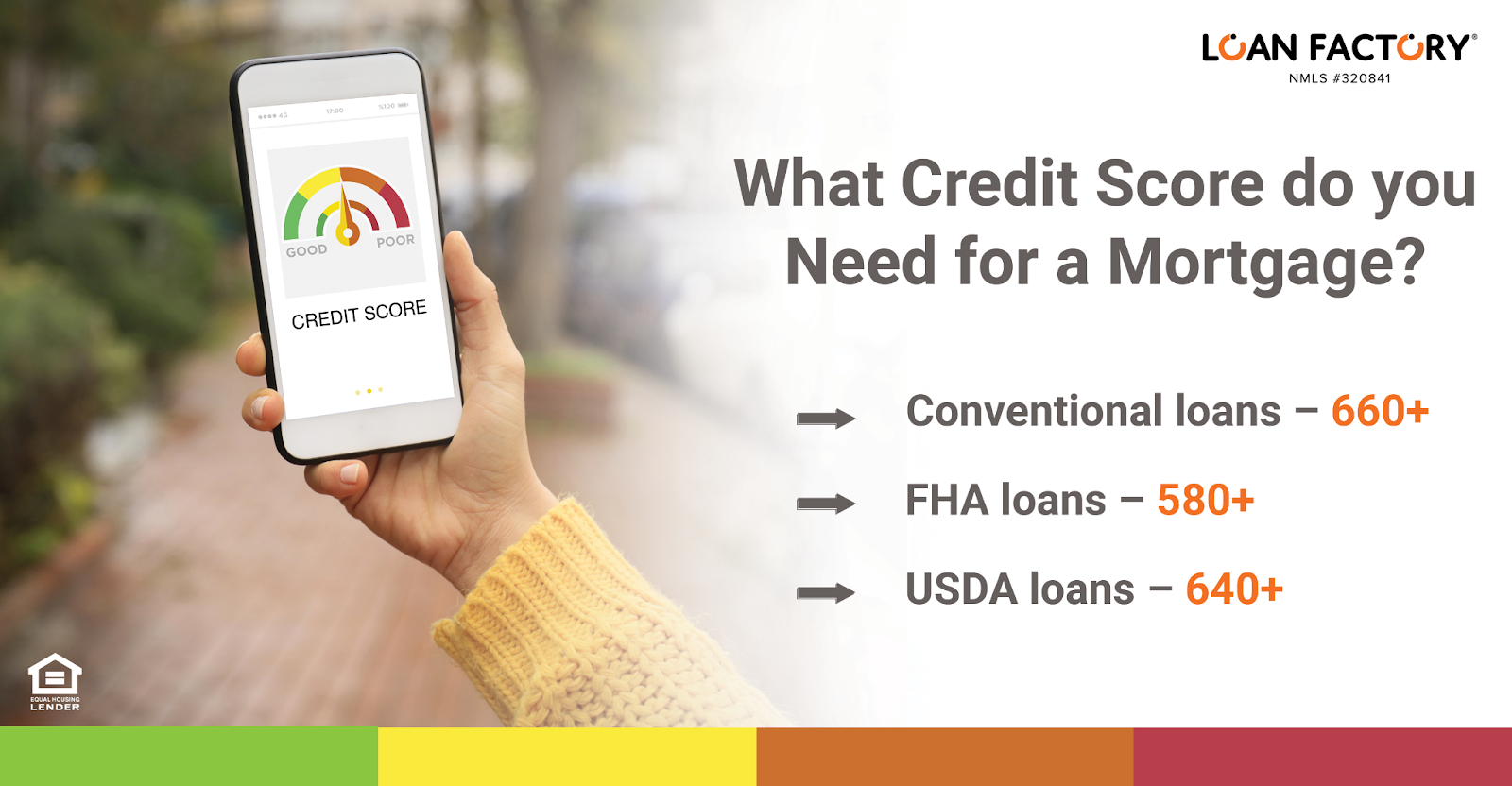

What Credit Score do you Need for a Mortgage?

Now that you know how important credit scores are for a mortgage let’s look at what credit scores you need for each loan program.

Conventional loans – 660+

FHA loans – 580+

USDA loans – 640+

However, these are the minimum credit score requirements. For example, if you have a 580 score and apply for an FHA loan, you’ll likely get a higher interest rate than a borrower with a 640 credit score. The key is to have as high of a credit score as possible.

Ways to Improve your Credit Score

Here are some tips to improve if you have a low credit score or one that doesn’t give you access to the lowest interest rates or fees.

Pull your Free Credit Report

To see what creditors report about you, pull your free credit reports. Everyone gets free access weekly, so you can check back often to see if your efforts paid off. Your credit report won’t show a credit score, but you’ll see your credit history and what you must change.

Fix your Payment History

If you have late payments, get them paid as quickly as possible. Your payment history is the largest part of your credit score. Bringing your payments current will increase your score quickly and give you access to better interest rates and lower fees.

Lower your Credit Utilization

Your credit utilization compares your outstanding credit to your total credit line. Ideally, you shouldn’t have over 30% of your credit line outstanding. Pay your balances down as much as possible if you have more than $300 for every $1,000 in credit line outstanding. In addition, lowering your utilization rate will increase your credit score.

Dispute any Errors

If you notice errors on your credit report, dispute them. Write a letter to the credit bureau reporting the information and explain why you think the information is incorrect. Provide as much proof as you can. The credit bureaus have 30 days to review the information and decide.

Take Care of Collections

If you have any collections on your credit report, try taking care of them. If you satisfy them, try negotiating with the collection agency to remove the tradeline from your credit report to allow your credit score to improve.

Final Thoughts

Your credit score greatly affects your mortgage. Improve your credit score if you’re trying to keep your mortgage rates and fees down.

You don’t need perfect credit, but the higher your credit score is, the less risk you pose to a lender. If you can provide a good credit score, a decent debt-to-income ratio, and a good down payment, you’ll increase your chances of securing the best interest rates and fees on a mortgage.